How to Make a Million Dollars: Myths about Real estate and owner financing.

So people think you need a lot of money to buy a house. But actually in many areas in the country you can get something for 1% down with owner financing or a FHA loan. These are starter homes, but if you get one and fix it up or add units you can gain a lot of wealth in the long run. here is how:

You may think you need a pile of cash to buy a house. A big fat 20% down, perfect credit, a banker who likes your face. And because they think that, they never start. They wait. They rent for fifteen years and hand a landlord a few hundred grand they're never getting back.

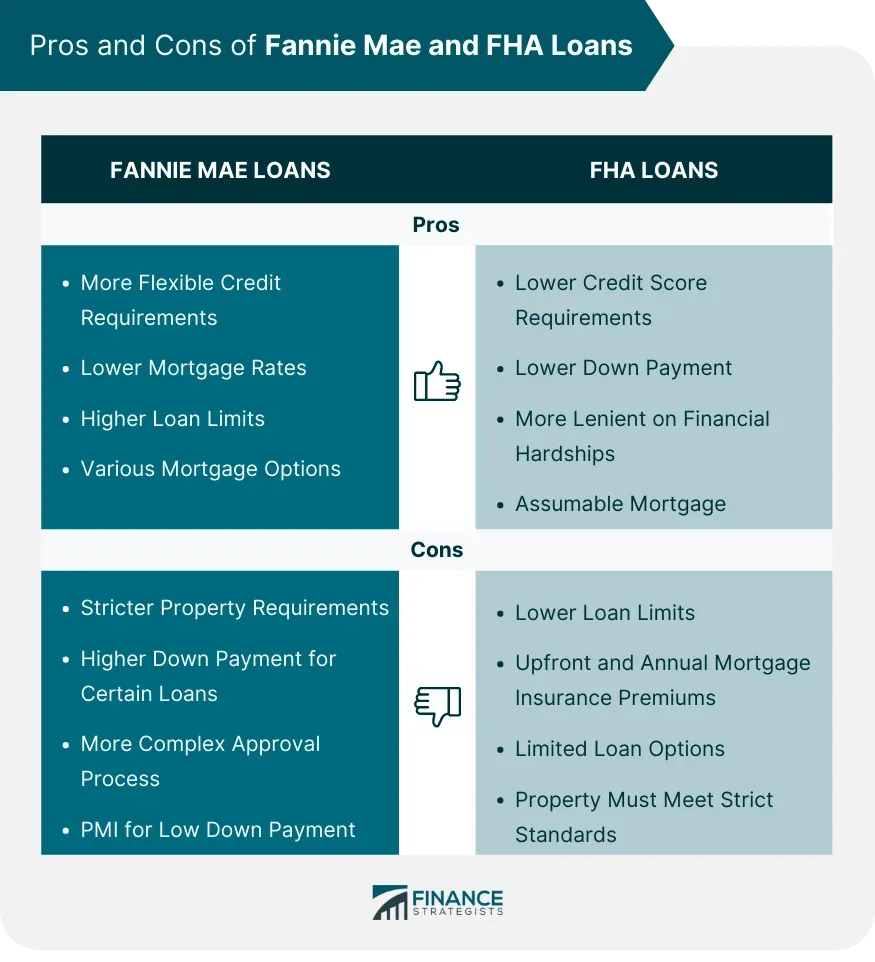

Here's the thing: it's mostly a myth. In a lot of the country you can get into your first property for almost nothing down — 3.5% with an FHA loan, sometimes 1–5% (or creative terms) with owner financing. These are starter homes, sure. Nothing glamorous. But if you get one, fix it up, maybe add a unit, and then do it again a couple years later, you can quietly build a million dollars in net worth over 10–15 years without ever earning a banker's salary. Let me show you how.

The myth that keeps you renting

The big lie is that real estate is for rich people. It's actually the opposite — real estate is one of the only games where the bank (or the seller) hands you most of the money to buy an asset, and then your tenants pay that money back for you. You put in a little. Other people's money does the heavy lifting. That's the whole trick, and almost nobody explains it plainly.

The second lie is that you need to be a contractor or a genius. You don't. You need to understand four engines, buy one okay property, and be patient. Patience is the part nobody wants to hear.

The tools (in plain English)

FHA loans. Government-backed, made for regular people. Around 3.5% down. And here's the move most folks miss: FHA lets you buy up to a four-unit building as long as you live in one unit for a year. So you can buy a fourplex, live in one, and rent the other three — that's called house hacking, and it's the single best starter move there is.

Owner financing. This is where the seller becomes the bank. Instead of you getting a mortgage, the seller lets you pay them monthly, with interest, on terms you both agree on. Down payment, rate, length — all negotiable. No bank breathing down your neck, faster closings, and you can often get in for way less down than a bank would ever allow. More on this below, because it's the most misunderstood tool in the whole kit.

House hacking. Living in the thing you bought while it pays for itself. Rent the other unit, rent the rooms, finish the basement and rent that. The goal is simple: get your housing cost to near zero so every dollar you would've paid in rent goes toward building YOUR wealth instead.

The first house: what it actually looks like

Let's get concrete. Say you find a tired little duplex in a normal town for $280,000.

- FHA, 3.5% down = $9,800. Throw in closing costs and you're all in for maybe $13–15k. (And a chunk of that you can often get the seller to cover.)

- Your payment — mortgage, taxes, insurance — is, say, $1,900 a month. You live in one side and rent the other for $1,300. So your actual housing cost is $600 a month. You just cut your rent by two-thirds on day one.

- Over that first year you paint, swap the ugly carpet, clean up the yard, maybe finish a basement room. Nothing fancy. The place is now worth $315,000. You just created about $35,000 in equity with a few weekends and a few thousand bucks.

That's the seed. Now watch how it grows.

How the money actually grows (the four engines)

This is the part that makes a million dollars feel boring and inevitable instead of magic:

- Appreciation. Real estate roughly trends up over time — call it a modest 3–5% a year. On a $300k house that's $9,000–$15,000 a year you didn't lift a finger for. Own a few houses and that number gets loud.

- Loan paydown. Your tenants' rent pays down your mortgage. Every month a little more of the loan becomes equity that belongs to you. Early on it's $5–7k a year per property; later it accelerates. Free money, paid by someone else.

- Forced equity. The renovation and the added unit — turning $280k into $315k. You manufacture this on purpose. It's the fastest equity there is.

- Cash flow. Once you move out and rent the whole place, it puts a few hundred dollars a month in YOUR pocket. You don't spend it. You stack it for the next down payment.

Four engines, all running at once, on every property you own. Now you just need more properties.

The snowball: a 12-year plan to a million

Here's a realistic arc. Conservative numbers, normal markets, no lottery tickets:

- Year 0: Buy House #1 (the duplex), ~$13k in. Live in it, fix it.

- Year 1–2: Move out, rent both sides. It now cash flows ~$400/month. You save that plus your normal savings.

- Year 2–3: Buy House #2 with another low-down loan. Repeat the house hack.

- Year 4–6: Buy House #3 — this time off-market, with owner financing, because now you understand it.

- Year 7–9: Buy House #4. Maybe add an ADU (a little backyard unit) to one of your earlier places to force more equity and more rent.

- Year 10–13: Buy House #5, keep improving the others.

Roll it forward 12–15 years and you're looking at something like five properties worth a combined ~$1.6–1.8 million, with maybe ~$850k still owed on them. That's $800k–$950k of equity that grew mostly on autopilot — and you're collecting a few thousand a month in cash flow on top. Add your reinvested cash flow and a couple of well-placed ADUs and you cross the million-dollar line. Not in a year. Not from one clever deal. From one okay house, repeated, with the four engines doing the work.

Owner financing: the most misunderstood tool there is

People hear "owner financing" and assume it's only desperate sellers or sketchy deals. Wrong. The best owner-finance sellers are usually older folks who own a place free and clear, are tired of being landlords, and would love a steady monthly check instead of a big tax bill from selling all at once. You solve their problem, they solve yours.

How it works: you and the seller agree on a price, a down payment, an interest rate, and a term. You pay them monthly like you would a bank. That's it. No loan officer, no underwriting committee, and terms you can actually negotiate — sometimes a tiny down payment, sometimes a few years before any big payment is due.

The catch — and you have to respect it: watch out for balloon payments (a big lump sum due down the road), get everything in writing, record it properly, and use a real estate attorney to paper the deal. This is the one place not to wing it. A good attorney costs a few hundred bucks and saves you from a few-hundred-thousand-dollar mistake.

Keeping it real

I'm not going to sell you a fantasy. Properties have bad months — vacancies, broken water heaters, a tenant who won't pay. Markets dip. Some of your "great deals" will be mediocre. This is slow money, not fast money, and it rewards people who don't panic and don't sell at the bottom. If you want overnight, go buy a lottery ticket. If you want a million dollars while you sleep, you buy boring houses and you wait.

But the myth — that you need to be rich to start — that one's just false. You need one starter home, a little nerve, and the patience to let the four engines run. Most people never start because they're waiting to be ready. Don't wait. Start small, start ugly, start now.

Why not pull the first deal up today?

Till next time,

-Bob (The Builder)

(Just my experience and how I think about it — not financial or legal advice. Run your own numbers and talk to a real estate attorney before you sign anything.)